TLDR: Australian's are likely facing shortfalls in diesel between 5% and 63% within weeks.

Australia is one of the most vulnerable countries to a liquid fuel emergency, as a small player at the end of the line in a complex supply chain. This analysis focuses on diesel due to its significance in agriculture and road freight.

See the web version for charts and links to the sources.

Global consumption of oil is approximately 105 million barrels per day (Mbpd). Australia uses about 1.1 Mbpd or 1% of the global total.

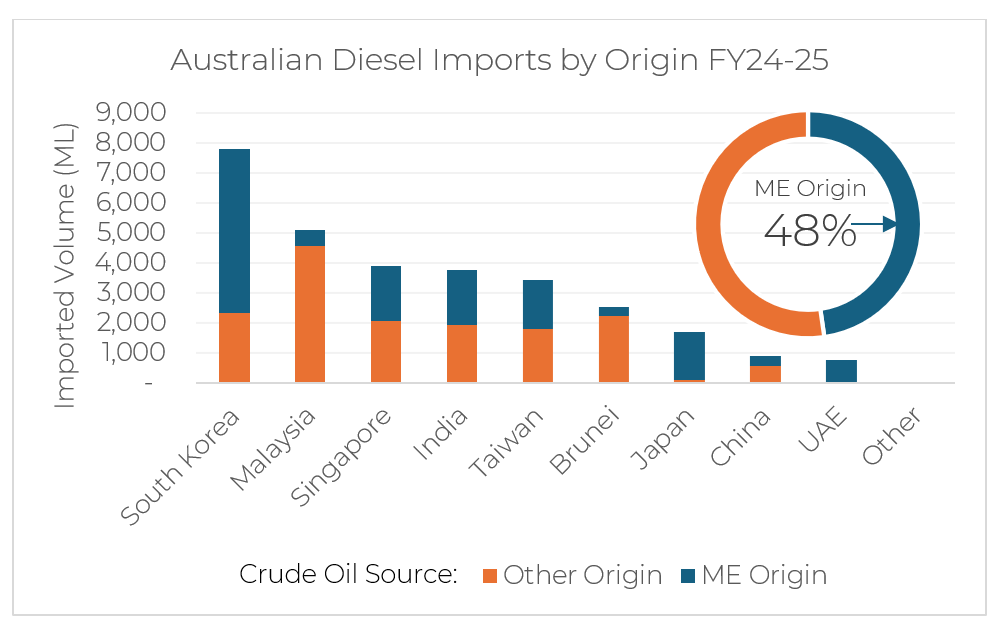

Only a small fraction of Australian diesel imports come directly from the Middle-East with the majority from Asian refineries. However at least 48% of the feedstock originates in the Middle-East while Malaysia, Brunei and China have substantial domestic production. This is only tracing back one layer. It is likely that with recursion effects, we would find an even greater portion of total supplies originate in the Middle-East.

Australia imported a total of 33,500 ML of diesel in 2025. Domestic production added an additional 4,500 ML from 17% local and 83% imported oil. More than 90% of this was used domestically. Australia extracted about 15,000 ML of crude oil and condensate for export (~0.26 Mbpd).

It is impossible to guess what direction the conflict will take next. A look at possibilities can help establish book-ends and the potential implications. This uses the import and consumption data of diesel from 2024 and 2025, levelised across the year, to make rough models, starting from the current reserve stock levels. Most of this data is sourced from the excellent Power BI data interface from the Australian government.

Best Case – Unrealistic

Events: The war ends tomorrow. The unaffected gulf states resume export at 80% of pre-conflict rates. Power is miraculously restored to the Iranian export facility on Kharg Island within one month. Refiners draw on emergency reserves to supply full demand for refining. Damaged infrastructure is repaired at the balance of plants within two months, restoring full production capability. All Australian production is retained in Australia and all shipments enroute to Australia arrive.

Implications on Australia’s fuel supplies: In this case reserve stocks are initially increased thanks to the retained Australian production. After enroute and allocated stocks arrive, a shortfall of 5% draws down the reserve stocks until imports resume in mid-May. Domestic production continues to be retained to increase stocks. Restrictions seem unlikely except to counter hoarding affecting farmers and remote consumers. Prices are likely to continue to rise with uncertainty until full supply is returned.

Moderate Case with Fair Distribution

Events: Conflict remains ongoing, but Middle East production continues at full bypass capacity of 43%. Refiners operate at 92% of pre-conflict levels and continue to supply Australia with the same share of total production as pre-conflict. 92% of Australian production is retained in Australia. Middle East production is restored after four months.

Implications on Australia’s Fuel Supplies: Once the refined products enroute and allocated to Australia have been used we see a 26% shortfall in supply. With no change in consumption, the stock will be depleted by mid-July. At that point there will be no choice but to reduce consumption to match available production. Prices of refined products are likely to see increases in the order of 400% based on the historical precedents. Examples include the 1973 oil crisis and the 2022 natural gas restrictions following Russian invasion of Ukraine.

Prolonged Severe Shortage and Hoarding

Events: All Middle-East production and/or export facilities are incapacitated. Refineries elsewhere prioritise domestic consumption, reducing stocks available to Australia to 50% of pre-conflict levels. Half the stock enroute to Australia is redirected before arrival. Over a period of five years, refineries are recommissioned to handle greater portions of oil from other sources.

Implications on Australia’s Fuel Supplies: A shortfall of 63% without demand management will see reserves depleted by the start of May. The Government is likely to declare a Liquid Fuel Emergency which allows for significant intervention in a range of ways as set out in the Liquid Fuel Emergency Guidelines 2019.

Severe restrictions will be likely to ensure prioritisation of military, freight and essential services as set out in these guidelines.

What about the 90 day IEA obligation?

Australian government and industry representatives have repeatedly assured the public that fuel won't run out. Ministers have stated that they are in the process of securing supplies. Yet, the only additional supplies mentioned anywhere are not supplies at all, but existing reserve stock.

The International Energy Agency (IEA) requires net-importing member countries to hold 90 days worth of net oil imports to help stabilise global supply. By this measure Australia has approximately 49 days as of December. This includes supplies on the water and overseas allocated to Australia, averaged across all petroleum products. Australia is one of only two IEA member countries to hold less than the obligated reserve stock. The reported reserve of diesel currently available is 26 days worth of consumption.

What can we do about it?

It is worth considering both short-term financial implications and probable direct restrictions on travel for anyone in Australia or similarly affected countries.

- Do you have a bike for everyone in your household?

- Are they in working order or do you know someone who can fix it for you?

- Do you know how to safely get to your key activities without a motorvehicle?

- Do you know which public transport options are available to you?

- What services are available closer to home?

- How well do you know your neighbours?

- Are you set up to work and/or school from home?

Further resources

Source: LivingMoreWithLess

6 Comments

There is one more thing you can do about it; switch Battery Electric Vehicle. Yes, its not a cheap option and it won’t be available to everyone, but EVs are not as expensive as they used to be. You can plug them in at home and off you go, no long overseas supply chains for consumable energy in your car or truck (yes there are truck based EVs all the way up to prime mover) and electricity is so much cheaper than dino juice per km travelled.

Those Gold Coast residents who actively campaigned to prevent the expansion of the tram network should be the first on fuel rations. With bans on using their 4×4.

I read this report it’s very well done

This is all very well in cities that have excellent public transport networks where residents can get to work, within relatively short distances but what about the regions? lol

I know of independent truckies that drive 1300km per shift. How will they afford to buy diesel?

Farmers need to sow crops very soon. How do they keep prices down, for us end consumers, when they need to pay more for everything in agricultural production?

This crisis has been a longtime in the making and the morons in Canberra, seem to be oblivious to conditions on the ground for most Australians.

The Federal Government needs to subsidise Australians and help us all out with sensible policies that help everyone.

Do we really need nuclear submarines in 50 years time, when the pollies are all dead?

Where is Australia’s long term strategic partner, USA, to help us when we need their prioritisation now?

All fuel destined for Australia has been delivered so far. Where are pulling a shortage from? Sound like the msm blah blah blah

Thanks OP, that was a great read. Ive been chatting with friends, some family members & collegues, who all expressed how they yearn for this war to end…i mean most of us do however ive been telling them not to expect fuel prices to drop. These fuel prices will hang around even after the israeli/yank war. It could take months if not a year to see any significant drop in fuel prices at the pump. Does OP agree?