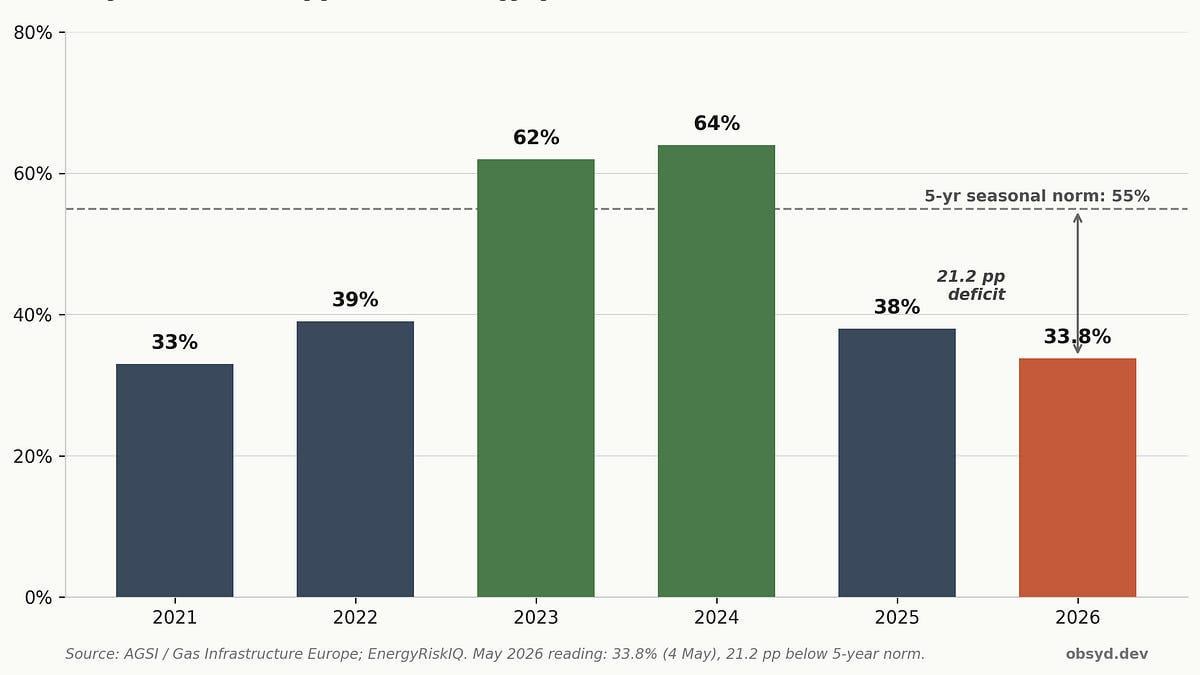

EU gas storage entered May at 33.8% of working capacity. The 5-year seasonal norm for this date is 55%. That’s a 21.2 percentage point deficit — the widest spring exit since 2018.

To meet the EU Commission’s 80% by 1 November target, the system needs sustained injections of roughly 2.85 TWh per day for the next 181 days. That rate is achievable in a normal year. 2026 is not a normal year.

Three structural constraints on the supply side:

Norway is at production plateau. Output peaked at 124 bcm in 2024, slipped to 120 bcm in 2025. Equinor’s CEO has publicly stated zero spare capacity. New volumes from Troll Phase 3 Stage 2 don’t arrive until end-2026.

2. Qatar is impaired. The 2 March Iranian strike on Ras Laffan removed approximately 17% of Qatari export capacity. Force majeure was declared 4 March. Industry estimates point to multi-year repair timelines.

3. Russia is on a phase-out clock. Pipeline transit through Ukraine ended 1 January 2025. EU LNG imports from Russia are banned from 1 January 2027. Russian gas isn’t a solution for the 2026 refill.

So Europe’s marginal cargo is increasingly US LNG. But US LNG can also clear into Asian markets at higher prices. JKM is currently $16.02/MMBtu vs TTF at $14.80. If TTF falls materially below €45/MWh, US-origin Atlantic-basin cargoes redirect east.

The closer historical parallel isn’t 2022 (war shock) but 2021 — when storage entered May low, Asia bid for cargoes, Gazprom underdelivered, and TTF rose from €19/MWh in January to €130 in December. All before any war.

If the 80% target stays binding, TTF is unlikely to sustainably reset below €45/MWh through Q3 2026.

Wrote up the full analysis with 7 charts, including the 2021/2022/2026 storage comparison and the cost asymmetry from the last crisis: https://obsyd.substack.com/p/european-gas-there-is-no-cheap-refill

Source: SpeakerOld4909