This post is related to the proyection of copper bottleneck for the next decade due to the electrification process and the fast development of data centered. Energy transition is going to need a staggering amount of copper: grids, EV motors, wind, solar, batteries, data centers, all expanding at once. We usually optimistically reply "well, we'll just substitute it."… Aluminum, carbon nanotubes, superconductors, new battery chemistries.

I've spent a while now reading through the actual literature on this topic and I think the framing is somehw broken. "Replacing copper" isn't one single question, but at least four, and they live on completely different timelines, with completely different physics, completely different economics, and completely different industries.

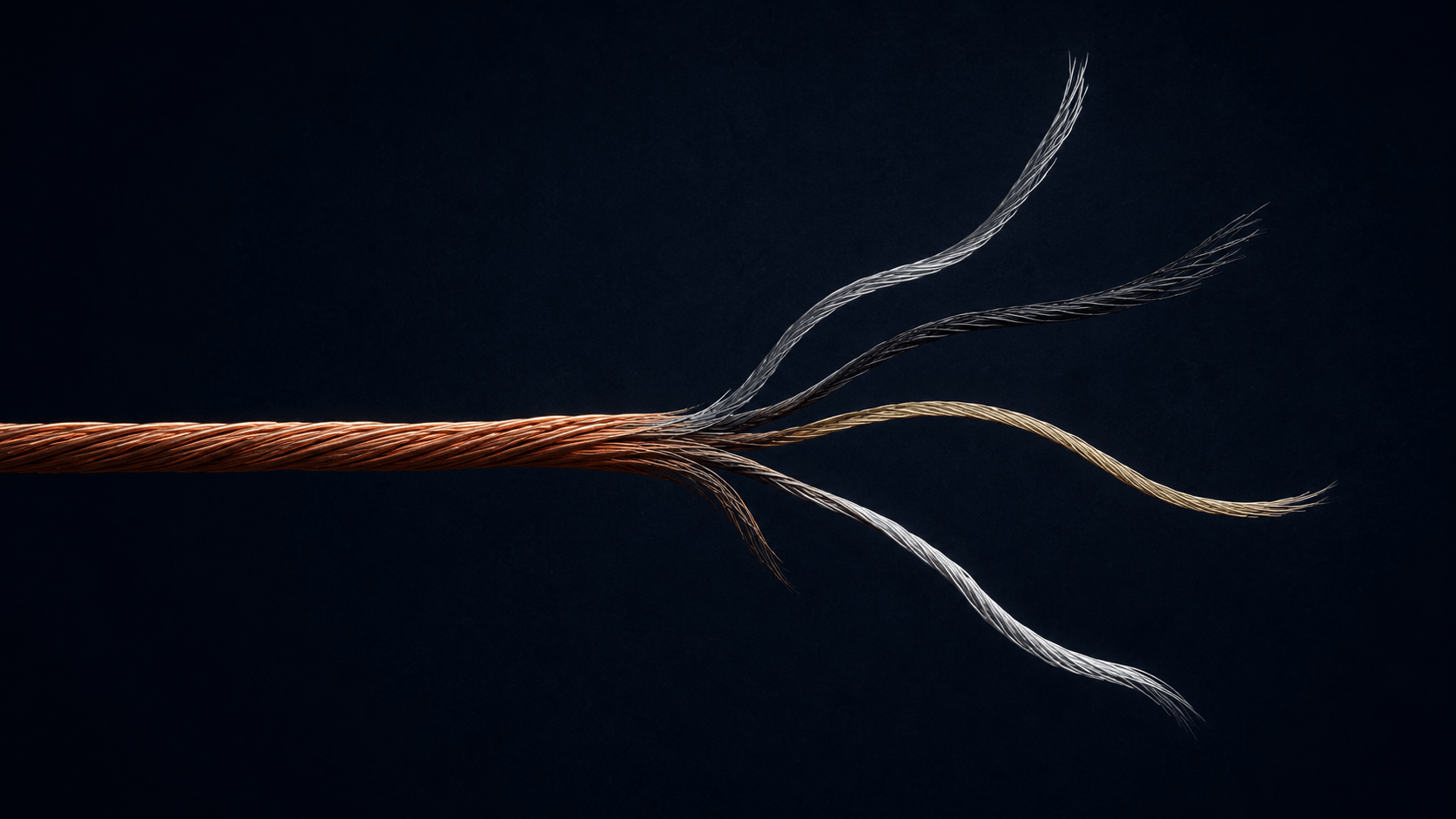

Here's an overview.

1. Aluminuim for mass substitution in conventional conductors: that´s mature

This is the boring one, and the only one that's actually deployed at scale. Aluminum has 61% the conductivity of copper by volume but about 30% the density, so for the same current you need a cable roughly 1.6× the cross-section, and it's lighter overall. Overhead transmission lines are already almost entirely made of aluminum. Along with most transformer windings. The EV wiring harnesses are in an active transition, for example BMW with TU München worked out how to handle aluminum's creep problem by turning it into a self-stabilizing feature with wedge-geometry contacts. Sumitomo Electric and AutoNetworks have, on the other side, shipped aluminum-alloy automotive conductors.

But the International Copper Association's own survey shows only about 1.3% of annual copper consumption is being replaced per year, mostly by aluminum. Small, stable, but slow. And the reason isn't price, indeed there's a 2025 econometric study showing consumers do shift back and forth with aluminum prices, but the magnitude is modest. The real brake is mostly sunk cost: every copper-based design is paired with copper-qualified terminals, connectors, training, regulatory compliance, machinery.

And aluminum isn't for "free": the primary aluminum production is 4–5× more energy-intensive per ton than copper refining. The carbon math gets recovered over a vehicle's lifetime through weight savings, but it's not automatic and it's not immediate.

2. Carbon nanotubes for substitution in weight-critical applications_ still niche and pre-commercial

CNTs have spectacular intrinsic properties at the single-tube scale, but the problem is that a real cable needs millions of nanotubes packed together, and once you do that, the conductivity collapses, because electrons have to hop across imperfect contacts between tubes instead of running cleanly down a single channel.

The best pure CNT fibers reach about 3% of copper's conductivity. Acid-doped, reached around 19%. Only polymer-doped fibers have hit 98%, which in my opinion is genuinely impressive, but the dopants tend to degrade with humidity and thermal cycling, so long-term reliability is an open question. A Korean lab built a fully metal-free electric motor with CNT windings in 2025: it ran at 94% the speed of a copper equivalent, which is a remarkable demo. But the CNT conductor cost is roughly $375–500/kg against copper's $10–11/kg. That's a 40× price gap, which no normal learning curve closes in a decade.

However, good news, there's a real industrial trajectory (a Houston company called DexMat is partnering with Prysmian on high-voltage cables based on their Galvorn fiber), but I don´t think this is "a 2030 grid solution". It's likely an aerospace and high-performance niche play for a long time, with maybe spillover to specific high-value applications.

3. Architectural redesign: sodium-ion batteries and high-temperature superconductors.

I find this is an interesting category, because the substitution isn't material-for-material. It's "change the system so the copper isn't needed in that function anymore."

In lithium-ion batteries, the anode current collector has to be copper because aluminum alloys with lithium at low potentials and destroys the collector. Sodium doesn't have that problem, so sodium-ion cells use aluminum on both sides. That's roughly two-thirds of the collector-cost saved per cell, and a meaningful chunk of copper demand quietly disappears at scale. CATL launched their Naxtra sodium-ion battery for mass production in April 2025, with 175 Wh/kg and over 10,000 cycles. But another company (Natron Energy) folded in September 2025. So the tech is real, but the business case is brutal.

High-temperature superconductors are the other piece. They operate in liquid nitrogen at 65–77 kelvin, can carry roughly 200× the current density of conventional resistive copper cables. A single HTS cable can exceed 3 GW. AmpaCity in Essen (Germany) has been running a 1km HTS link in a live distribution grid since 2014. While Airbus is developing a 2 MW superconducting propulsion demonstrator for hydrogen aviation. Further, the global HTS power cable market was about $174M in 2024 and is projected to hit $578M by 2032. Small, but real, mostly justified where space, weight, or power density compensate for the cryogenic cost. Probably a niche-grows-to-medium story over 20 years.

4. Nanoelectronic interconnects: topological semimetals, far-horizon but strategically loaded. Honestly, my favourite one.

This one barely gets discussed outside materials journals and I think it's the most interesting.

Inside an advanced chip, transistors are wired together by copper interconnects. As linewidths shrink below ~5nm, copper stops behaving like copper. Surface and grain-boundary scattering dominate, the resistivity climbs sharply, and the effective conductivity can collapse by a factor of ten. The barrier liner you need to keep copper from diffusing into the dielectric eats more of the cross-section the smaller you go. This is a hard physical ceiling on chip scaling and it's hitting right now.

But…

A 2025 paper in Science showed that ultrathin niobium phosphide films (a topological semimetal where electrons travel along protected surface states with almost no scattering) outperform copper at sub-5nm thicknesses, even though bulk NbP conducts about 20× worse than bulk copper. The thinner the film, the better it does, which inverts the usual intuition. And the films don't have to be single-crystal, which makes a real fab process at least imaginable.

Wha all this matter?

Well, under the S&P Global 2026 projection, copper consumption from data centers alone roughly doubles by 2040. The AI buildout is putting enormous pressure on chip-grade conductors at precisely the moment the rest of the energy transition is competing for the same material base. A partial materials substitution at the most advanced nodes wouldn't show up as huge tonnage, but the strategic leverage is large: a few grams in the right layers of a leading-edge chip is worth a lot.

This post is a summary of a deep dive with more than 20 original references, including peer reviewed articles.

Source: raw-science

1 Comment

So you finally did your homework and discovered for the largest volume users cheap and abundant aluminium is perfectly fine.

As we explained when you started this series 2 months ago.